The financial advisor career path

When considering a career as a financial advisor, there are four distinct paths to take. Each path offers its own unique opportunities and challenges, so it’s important to carefully consider which one is the best fit for you.

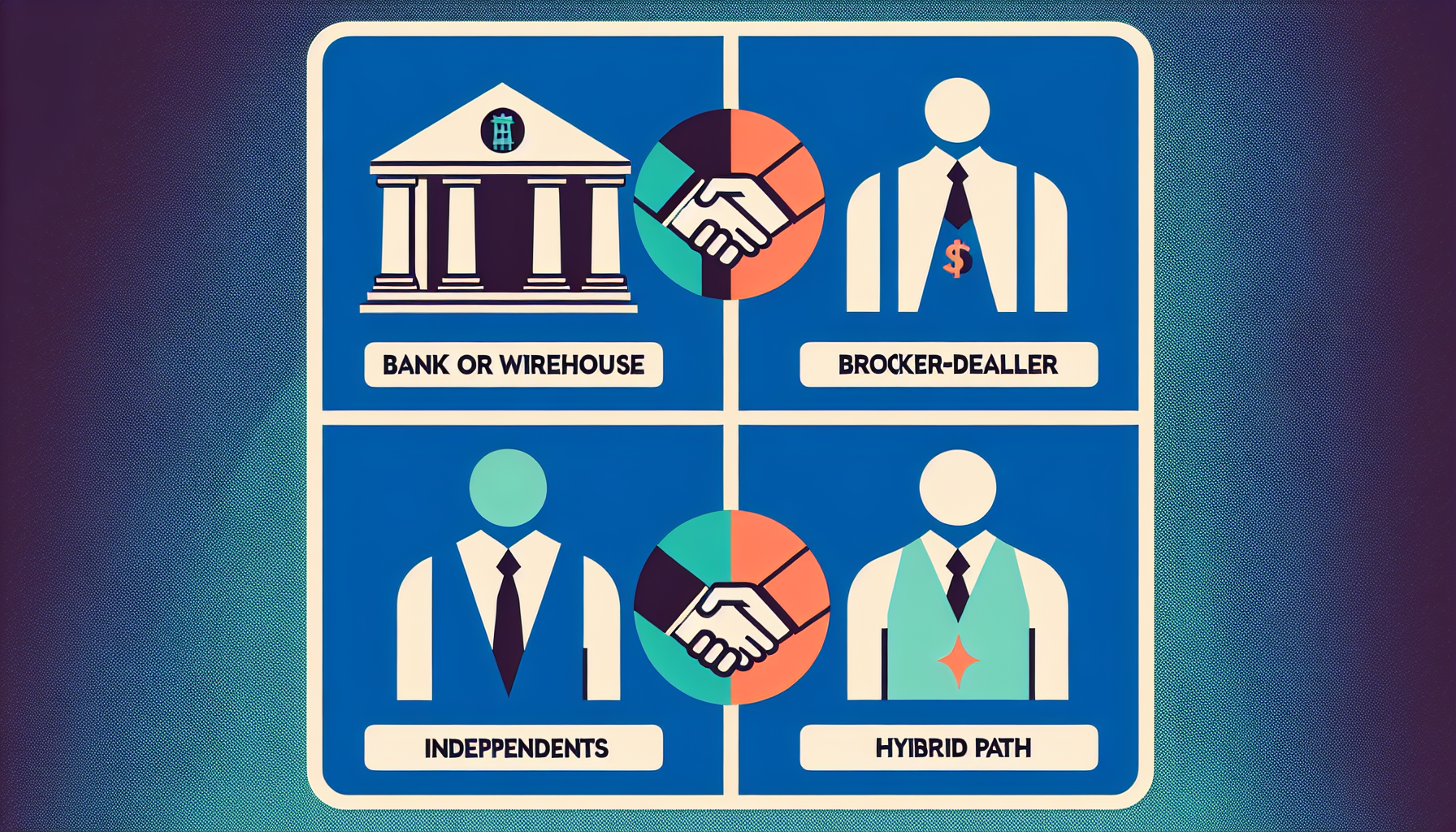

The four paths into the financial advisor career include:

- Bank (or wirehouse/captive)

- Broker-dealer

- Independents (or registered investment advisors)

- Hybrids

There are differences between each channel. They are the bank (or wirehouse/captive), broker-dealer, independents (or registered investment advisors) and hybrids

Each channel in the financial advisor industry has its own unique characteristics and requirements. Understanding the differences between each channel can help you make an informed decision about your career path.

Bank (or wirehouse/captive)

This channel includes large institutions like Morgan Stanley, Goldman Sachs, and Merrill Lynch. These firms often have structured programs for new advisors and offer the opportunity to work with a well-known brand.

Broker-dealer

Advisors in this channel work for firms that sell investment products and services. They must be licensed to sell these products and often represent the interests of the firm over the client.

Independents (or registered investment advisors)

Independent firms are usually owned by a single individual or partners. Advisors in this channel may have more flexibility and control over their practice, with a focus on providing advice rather than selling products.

Hybrids

Hybrids offer a combination of the broker-dealer and independent models, allowing advisors to provide financial services, charge fees for advice, and sell products. This model presents a unique blend of opportunities and challenges.

There is a different standard in those channels—it is the suitability standard or the fiduciary standard

Each channel in the financial advisor industry operates under a different standard, namely the suitability standard or the fiduciary standard. The suitability standard is used by the bank, broker-dealer, and hybrid channels, while the fiduciary standard is common in the independent channel, registered investment advisors (RIAs), and hybrids to some extent. The fiduciary standard requires advisors to always act in the best interest of their clients, putting the client’s needs above their own. On the other hand, the suitability standard only requires advisors to recommend products that are suitable for their clients based on their financial needs, objectives, and unique circumstances. This standard is a lower standard and may not always align with the client’s best interests.

Advisors operating under the suitability standard may be more focused on finding a fit for a specific product, whereas those adhering to the fiduciary standard are focused on customizing financial advice and solutions to best serve their clients. It’s important to understand the difference between these standards, as it can greatly impact the type of advice and service you receive from a financial advisor.

Why you may choose either has totally to do with you and what you believe. Can you serve the client’s best interest using either standard? What you would do for your parents should be what you do for clients

Deciding which path to take as a financial advisor ultimately comes down to your personal beliefs, values, and ethical standards. When choosing a career path, the most important question to consider is whether you can serve the client’s best interest using either the suitability standard or the fiduciary standard. What you would do for your parents should be what you do for clients—always acting in their best interests and putting their needs first.

While each path—bank, broker-dealer, independent, or hybrid—has its own unique opportunities and challenges, the decision should be based on your own ethical compass. It’s essential to align your career with your personal values and beliefs, ensuring that you can provide the highest level of service and advice to your clients. Remember, the standard you operate under can greatly impact your ability to serve your client’s best interest, so choose a path that resonates with your core values and principles.

The securities industry essentials (SI e) exam

The securities industry essentials (SIe) exam is a gateway into the financial advisor industry that provides a refresher and in-depth understanding of the industry. This exam serves as a barrier to entry for those serious about a career in the financial industry, as employers may require candidates to pass this exam before considering them for employment.

Prior to the SIe exam, individuals were required to be sponsored by a firm before taking the series 7, 66, or 63 exams. However, the SIe exam now allows individuals to take the exam without being sponsored, providing a more accessible entry point into the industry.

Passing the SIe exam is essential for new entrants into the financial advising industry, laying the groundwork for further licensing and specialization. This exam serves as a foundational step for individuals looking to work for a firm or partner with an existing firm, providing a comprehensive understanding of the industry’s core concepts and requirements.

The bank (or wirehouse/captive) channel

The bank (or wirehouse/captive) channel in the financial advisor industry encompasses large institutions such as Morgan Stanley, Goldman Sachs, and Merrill Lynch. These firms offer structured programs for new advisors, providing opportunities to work with well-known brand names and serve a diverse client base.

Entering the bank channel often involves completing a program that includes obtaining necessary licenses and training to serve clients effectively. Advisors in this channel have the advantage of leveraging the reputation and resources of established financial institutions, offering a strong support system for new professionals.

Working within the bank channel allows financial advisors to access a wide range of financial products and services, catering to the needs of clients with diverse financial goals and objectives. This channel provides a foundation for advisors to establish credibility and build relationships within the industry.

The broker-dealer channel

The broker-dealer channel is an important pathway for individuals pursuing a career in the financial advisor industry. Here’s what you need to know about this channel:

What is it?

Advisors in the broker-dealer channel work for firms that sell investment products and services. They must be licensed to sell these products and often represent the interests of the firm over the client.

Opportunities and Challenges

This channel offers the opportunity to work with well-known firms like Morgan Stanley, Goldman Sachs, and Merrill Lynch. However, it also comes with the challenge of prioritizing product sales over customized financial advice for clients.

License Requirements

Individuals looking to enter this channel will need to obtain the necessary licenses, such as the series 7, 66, or 63 exams, which are essential for providing financial advice within the broker-dealer model.

The independent Channel

The independent channel in the financial advisor industry has gained popularity in recent years, offering a unique approach to financial advising. Here’s what you need to know about this channel:

What is it?

Independent firms are usually owned by a single individual or partners. Advisors in this channel may have more flexibility and control over their practice, with a focus on providing advice rather than selling products.

Advantages and Disadvantages

Independents allow advisors to prioritize the client’s best interest and offer customized financial advice. However, there may be fewer resources and brand recognition compared to large institutions.

Standard of Care

Advisors operating under this channel typically adhere to the fiduciary standard, always acting in the best interest of their clients. This commitment to the client’s needs sets independents apart from other channels in the industry.

The hybrid channel

The hybrid channel in the financial advisor industry offers a unique blend of opportunities and challenges. Advisors in this channel have the ability to provide financial services, charge fees for advice, and sell products. This model presents a combination of the broker-dealer and independent models, allowing for a diverse range of services and offerings.

Working in the hybrid channel provides financial advisors with the flexibility to tailor financial solutions to best serve their clients’ needs. It allows for a more comprehensive approach to financial advice, combining the benefits of product sales and customized financial planning services. However, it’s important for advisors in this channel to navigate the unique challenges and responsibilities associated with both fee-based services and product sales.

Advisors operating in the hybrid channel must carefully consider the best strategies for integrating product sales with personalized financial advice. Finding the right balance between these two aspects of the financial advising business is crucial for providing the highest level of service to clients.

The difference between the fiduciary standard and the suitability standard

Within the financial advisor industry, there are two primary standards that guide the practices of professionals: the fiduciary standard and the suitability standard. Understanding the differences between these standards is essential for both advisors and clients.

The Fiduciary Standard

The fiduciary standard requires financial advisors to always act in the best interest of their clients, prioritizing the client’s needs above their own. Advisors operating under this standard are obligated to provide advice and recommendations that align with the client’s financial goals and objectives.

The Suitability Standard

In contrast, the suitability standard only requires advisors to recommend products that are suitable for their clients based on their financial needs, objectives, and unique circumstances. This standard does not necessarily prioritize the client’s best interests and may lead to recommendations that are not fully aligned with the client’s financial goals.

Advisors who adhere to the fiduciary standard focus on customizing financial advice and solutions to best serve their clients, while those operating under the suitability standard may be more focused on finding a fit for a specific product. It’s important for clients to understand the implications of these standards, as they can greatly impact the type of advice and service they receive from a financial advisor.

The loyalty and standard differences between broker-dealers and independent firms

Each channel in the financial advisor industry operates under a different standard, namely the suitability standard or the fiduciary standard. The suitability standard is used by the bank, broker-dealer, and hybrid channels, while the fiduciary standard is common in the independent channel, registered investment advisors (RIAs), and hybrids to some extent.

Advisors working for a broker-dealer are typically held to a suitability standard, which means their loyalty is to the firm they represent. They prioritize finding a fit for a specific product over serving the client’s best interests. This standard is considered lower, as it focuses on meeting the client’s financial needs rather than customizing financial advice.

On the other hand, independent firms, RIAs, and hybrids to some extent operate under the fiduciary standard. This higher standard requires advisors to always act in the best interest of their clients, putting the client’s needs above their own and the interests of the firm. Advisors adhering to the fiduciary standard focus on customizing financial advice and solutions to best serve their clients, ensuring that the client’s best interests are always prioritized.

What are your thoughts on the suitability standard vs. the fiduciary standard?

Deciding which standard is preferable ultimately comes down to your personal beliefs, values, and ethical standards. The suitability standard may be suitable for those who prioritize product sales and are comfortable with representing the interests of the firm they work for. However, the fiduciary standard is ideal for advisors who prioritize serving the client’s best interest, always putting the client’s needs first and customizing financial advice to align with the client’s financial goals and objectives.

It’s important to carefully consider which standard resonates with your core values and principles. Ask yourself if you can serve the client’s best interest using either standard and whether the standard you choose aligns with your personal beliefs. Remember, the standard you operate under can greatly impact your ability to serve your client’s best interest, so choose a standard that aligns with your ethical compass and commitment to serving your clients.

Why would you choose either one of those four paths

Deciding which path to take as a financial advisor ultimately comes down to your personal beliefs, values, and ethical standards. When choosing a career path, the most important question to consider is whether you can serve the client’s best interest using either the suitability standard or the fiduciary standard. What you would do for your parents should be what you do for clients—always acting in their best interests and putting their needs first.

While each path—bank, broker-dealer, independent, or hybrid—has its own unique opportunities and challenges, the decision should be based on your own ethical compass. It’s essential to align your career with your personal values and beliefs, ensuring that you can provide the highest level of service and advice to your clients. Remember, the standard you operate under can greatly impact your ability to serve your client’s best interest, so choose a path that resonates with your core values and principles.

Considerations before starting your own financial advisory firm

Before starting your own financial advisory firm, there are several important considerations to keep in mind. This decision requires careful planning, preparation, and a clear understanding of the responsibilities and challenges that come with entrepreneurship in the financial industry.

Educational and Licensing Requirements

Ensure that you have the necessary educational qualifications and licensing requirements to operate as an independent financial advisor. This may include obtaining the appropriate licenses, such as the series 7, 66, or 63 exams, and staying informed about industry regulations and compliance standards.

Business Plan and Financial Strategy

Develop a comprehensive business plan and financial strategy that outlines your target market, services offered, revenue streams, and growth projections. Consider seeking guidance from experienced entrepreneurs or financial professionals to create a viable business model.

Client Acquisition and Retention

Establish a plan for client acquisition and retention, including marketing initiatives, networking opportunities, and client relationship management strategies. Building a strong client base is essential for the long-term success of your advisory firm.

Compliance and Legal Considerations

Understand the compliance and legal requirements associated with operating an independent financial advisory firm. Stay updated on industry regulations, privacy laws, and client data protection to ensure full compliance with legal standards.

Technology and Infrastructure

Invest in the necessary technology and infrastructure to support your advisory firm’s operations, including client management systems, financial planning software, and cybersecurity measures. A robust technology framework is essential for efficient service delivery and data security.

Professional Networking and Partnerships

Build professional networks and strategic partnerships within the financial industry to enhance your firm’s credibility, access resources, and collaborate with other professionals. Networking can also lead to valuable referrals and business opportunities.

Starting your own financial advisory firm requires careful consideration of these factors to ensure a successful and sustainable business venture. With thorough preparation and a clear vision, you can embark on an exciting journey as an independent financial advisor, serving the best interests of your clients and contributing to their financial well-being.

FAQ

- What are the four distinct paths into the financial advisor career? There are four main paths into the financial advisor career: independent advisory firms, wirehouses (large brokerage firms), banks and credit unions, and insurance companies.

- How does the suitability standard differ from the fiduciary standard? The suitability standard requires financial advisors to recommend products that are suitable for their clients’ financial situations, while the fiduciary standard requires advisors to act in the best interest of their clients at all times, putting their clients’ interests above their own.

- What is the securities industry essentials (SIE) exam? The Securities Industry Essentials (SIE) exam is an entry-level exam administered by FINRA (Financial Industry Regulatory Authority) that assesses basic securities industry knowledge for prospective securities industry professionals.

- Why is it important to align your career with your personal values and beliefs? Aligning your career with your personal values and beliefs ensures that you are working in a way that is meaningful and fulfilling to you. It can lead to greater job satisfaction, motivation, and a sense of purpose in your work.

- What are the considerations before starting your own financial advisory firm? Before starting your own financial advisory firm, it’s important to consider factors such as regulatory requirements, business planning and strategy, target market and services offered, technology and infrastructure needs, as well as financial and operational considerations.